The reason, John Hussman states, that quantitative easing and other currency-related manipulations are not more effective on the economy is that they do not increase the velocity of money flowing around the economy.

He states (in Losing Velocity: QE and the Massive Speculative Carry Trade):

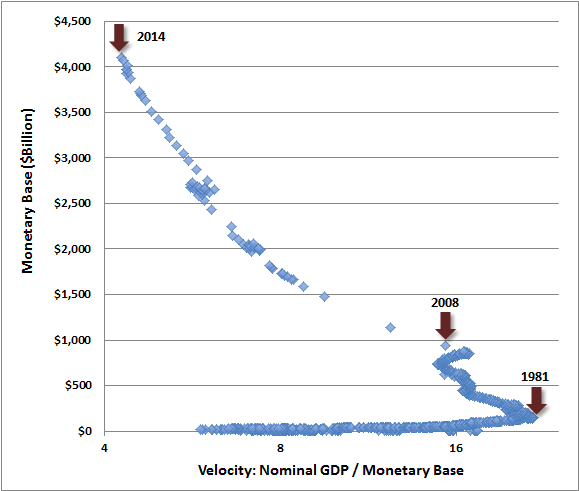

From a monetary perspective, it’s easy to understand why replacing Treasury securities with zero-interest money (currency and bank reserves) does little to “stimulate” the economy. We may wish to believe that putting more zero-interest money into the economy would lead people to go out and spend those idle balances, but that imagines some fixed ratio between economic activity and the amount of money outstanding. That’s the error. The velocity of money (nominal GDP / monetary base) isn’t fixed at all. What happens in practice is that as the Fed creates more zero-interest money, holders try to get rid of it by buying financial assets that provide a higher potential return – driving prices up and expected future returns down until they are indifferent between an overpriced financial asset and zero-interest money. The closest alternative to currency is Treasury bills. So as the Fed creates more zero interest money, investors bid up Treasury bills, which lowers their interest rate. That’s how Fed actions move short-term yields.

He also has included several charts, one of which compellingly exhibits this truth, compiled from Federal Reserve data compiled over the past century (or so).As the central bank creates more money and interest rates move lower, people don’t suddenly go out and consume goods and services, they simply reach for yield in more and more speculative assets such as mortgage debt, and junk debt, and equities. Consumers don’t consume just because their assets have taken a different form. Businesses don’t invest just because their assets have taken a different form. The only activities that are stimulated by zero interest rates are those where interest rates are the primary cost of doing business: financial transactions.

As you can clearly see, the velocity of money around the economy, which is a fundamental factor in real economic growth, is at historic lows. The relationship between the the zero-interest base money and the return potential made available by the higher interest investments is a primary driver in the velocity of money, and therefore, real economic growth.

Sadly, I doubt the Fed will choose to see or acknowledge this analysis enough to actually change course and perhaps aid the ailing economy that we find ourselves mired within.

No comments:

Post a Comment